Anyone who says they know what the future holds is trying to tell you a bill of good but one thing that we don’t spend a lot of time thinking about where we have come from. Of course plenty of ink has been spilled on the downfall (and revival) of the manufacturing sector the state of our economy and discussions of economic diversification. But there hasn’t in my opinion be a broader conversation where we have come from and are headed in the economic space.

First I am digging into some of the data that was originally posted by Mike Moffatt on SW Ontario manufacturing data and other employment and income data. I have decided to zoom in and unpack the specific context for the Windsor CMA (does not include Essex, Kingsville and Leamington in our region). Looking back 18 years to 2001, provide significant context to how our economy has evolved over the first two decades (nearly). Although there are predictions for the economy (nationally) to continue to pick up steam, moderate or go into recession in 2019 (no one actually knows what’s going to happen). Locally things are expected to moderate.

Employment

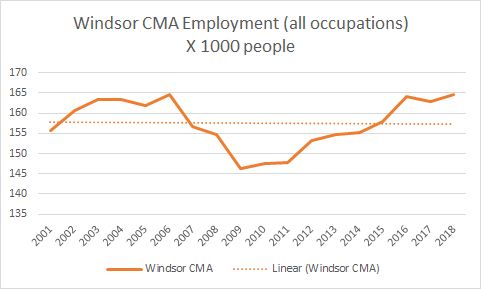

We know that our local economy has been growing over the last few years but understanding where we have come from is important.

The chart above shows a high of 164,500 persons employed in 2006, by the end of 2018 it had recovered to 164,400 persons. In the first 6 months of this year, employment rose to approximately 173,500 persons (based on a 6 month average of 2019) which is a new high for our community and region. The recession is clearly visible with the downward spiral occurring what I would call a traumatic 3 year period, bottoming out for 2 years before a long 5 climb to a return to relative prosperity.

Overall Windsor has seen a 5.6% employment growth between 2001 and 2018. If we include the first 6 month average of 2019 that value jumps to 11.5%. There are a lot of caveats in this number due to the month to month noise in the Labour Force Survey and the fact that this average only include 6 data points compared to 12 for the other years. So far 2019 has been a good year for our economy, which is an indicator of how strong our economy has been.

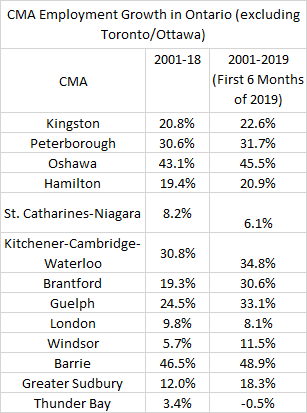

When we compare ourselves to the rest of Ontario (less Toronto and Ottawa) Windsor does find itself in the lower half of pack for employment growth. That being with that partial 2019 data we have outpreformed our comparative communities of London and St. Catherines. The addition of those Toronto and Ottawa metro areas doesn’t change Windsor’s standing that much but they have outgrown most of Ontario. That being said, the recession did hit Windsor hardest Windsor’s employment shrinking by 5.9% between 2001 and 2009. There is some likelihood in softening in the rest of 2019 with pending Chrysler third shift coming to an end. As a 1,000 persons employed equates to a 0.7% variation for percentage in the Windsor CMA could see the average regress back towards to mean over the rest of the year.

Sectors

In a previous post, spoke to our creative economy and where people live in our community. This data came from North American Industry Classification System (NAICS) codes that Statistics Canada tracks and how various job types/sectors have evolved over time.

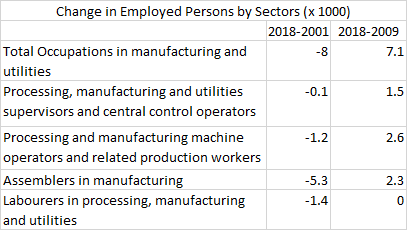

Due to some rounding, the values don’t quite add to the Total Employment numbers but you can see the change in employment from both 2001 and 2009 to 2018 by key sectors of the local economy. A number of insights can be gleaned from this. For example in occupations in manufacturing and utilities, despite a dramatic rebound since the depths of the recession (adding over 7,100 people employed since 2009) over it is still 8,000 people under the employment level in 2001. This was not only driven by a permanent loss in certain jobs ex. closure of the GM Trim plan, but also the role of automation in our local economy.

Another interesting category is the Trades, Transport and Equipment operators which has seen almost no significant growth in our community despite the reported high demand (here, here, and here). The revival of our economy explains the growth from 2009, but the anemic change since 2001 is concerning, particularly given the number of massive infrastructure projects in our community (Gordie Howe Bridge, Ambassador Bridge, Hospital) and the wide ranging initiatives that have attempted to drive people into a well paying and secure field of work.

Public Sector Economy

Since 2001, the largest growth sectors have been in have been in social service/education/legal areas and health care related fields which are largely publicly financed. It isn’t surprising that these public sectors have seen relative employment stability through the recession as employment stability tends to be higher in these sectors. The growth of these sectors are broken down blow:

There are many different angles you could view this data from. The margin of error decline in “front-line protection services” could be attributed to the retirement in local police forces not being rapidly replaced or the increase in nursing positions being driven by health care sectors beginning to shift to cope with an again work population; which also makes the decline in Professional Occupations in heath outside of nursing concerning.

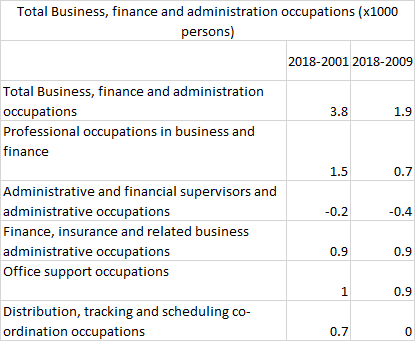

The highest area of growth from a “private” sector of our economy is in Business, Finance and Administrative occupations which are broken down below.

Despite almost equal total sector growth between two time frames. These sectors of all of those that are listed, are probably the least specialized. During the belt tightening of the recessions, admin assistance were a luxury that many companies probably couldn’t afford the supervisor role in these positions were hit, and never recovered, the support occupations have bounced back. Again despite there being latent demand in some of these sectors – like the logistics sector, shortages seem to remain the norm, with no significant growth measured between 09 and 18.

It is no surprise to anyone that manufacturing was hit hard with 8,000 jobs lost but where and what those jobs were do matter.

We know that over the long term there has been a decline in this sector. The rise of central control operators in the last decade points to the increasing automation as capital seems to be replacing labour. This automation places additional pressure on assemblers and labourers have in these sectors. As additional education and training are needed for these control positions compared to labour

An Economic Shift?

A conclusions that could be drawn the nature of our economy has changed. If we were to classify sectors between “public” sector vs “private” sector from Table 2 – with Health, Education/Social/Legal and Arts/Culture/Recreation being “public” and the remaining categories being “private”. You find that between 2001 and 2018 the public sector grew by approximately 10,800 people employed, while the private sector categories shrank by 2,600 employed persons. Obviously it isn’t as clear cut as I state above, due to the groupings used by Statistics Canada but the fact that in private sector employment growth has not kept up with public/social sector categories is an interesting dynamic for our community.

Looking at total employment these “public” sectors represent about 20% of our local employment, but they are the sectors that have grown fastest, had the most resiliency through downturns and the number of people making the “sunshine list‘ grows year over year (nearly 2,600 individuals in 2018 by my count).

Meanwhile our largest sectors like Sales and Services are largely stagnant in growth, pay significantly less and have much less stability in hard economic times. We know what the boom bust cycle of manufacturing brings. It is highly unlikely that the manufacturing 8,000 jobs that left this community over the last 18 years are coming back. Arguably it is more likely that the 18,000 jobs that remain will continue to decline as additional automation takes hold.

This is a conversation that really hasn’t played out in our community, the fact that we are becoming less a company/factory town and more of a public/social sector town. This seems to be resulting in stable employment seems to be tied more to a narrowing set of sectors in our community. As we look to diversify out economy, this public-private interplay is a factor that should not be ignored.